Imported from: Google Blogger site

Original publish date: September 4, 2017

The flexibility of bearer and registered bonds

People unfamiliar with out hobby tend to classify all certificates as 'stocks.' That is easy to understand because the nightly news always reports results of the latest trading day on the New York Stock Exchange but rarely mentions bonds. Nonetheless, bonds are highly important, both to corporate finance and our hobby. At the current time, 39% of all identified cataloged railroad certificates are bonds.

Understanding Bonds 101

Bonds were the primary sources of funds for many, if not most, railroad companies. While bonds seem mysterious at first, they are actually quite simple in concept. Bonds represent loans made TO companies.

The most common types of railroad bonds were mortgage bonds. Mortgage bonds are highly similar to ordinary mortgages on typical single family homes. In fact, railroad mortgages include many of the same conditions as home loans. Both types of mortgages are security agreements whereby mortgagors (borrowers) give mortgagees (lenders) the right to seize their collateral (property) if they default (cannot or will not pay) on their bonds (binding, written promises to repay.)

Bonds are written promises to repay at a specific future time. The two main differences between railroad mortgage bonds and home mortgages are, 1) companies must repay the entire principal on bonds at the time of redemption while homeowners pay some principal with every payment they make on home loans, and 2) foreclosing on corporate bonds is a much longer, more difficult process than foreclosing on home loans.

The need for more money and more flexibility. In the high-growth period following the American Civil War, companies came to realize that many of their bondholders demanded anonymity and freedom to exchange bonds with minimal intervention, while others wanted more security in their investments. Hence the reason that railroad companies increasingly turned toward issuing both registered and bearer bonds after the 1870s.

During that period, companies gradually lengthened the terms of their loans from twenty and thirty years to one hundred years and even longer. The longer the terms of bonds, the more certain that ownership of bonds would change before redemption. Consequently, companies realized they needed to let their bondholders change the statuses of their bonds between registered and bearer formats.

In order to embrace that concept, most companies allowed their investors to:

- register bearer bonds, and

- exchange registered bonds for bearer certificates.

The stories on the backs of bonds. Most bonds reserve spaces on the backs for recording transitions from one format to the other. Admittedly, most collectors spend little time looking at the backs of their certificates, not aware that the recorded transitions between bearer and registered status can give interesting insights into corporate histories.

Here are some examples.

Transition from registered status to bearer status.

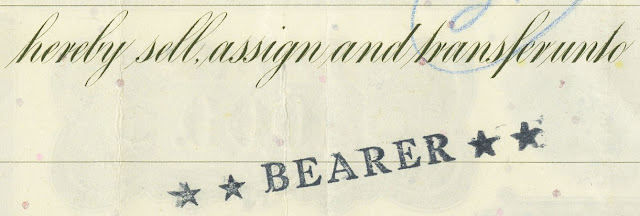

This investment started life as a registered bond when issued January 23, 1969. The assignment panel on the back of that bond is shown below and attests that the bondholder promptly converted the bond to bearer status on February 5, 1969, only thirteen days later! The assignment to 'Bearer' and the stamp would have been added by the Pennsylvania Railroad Company. Although clearly labeled as a 'registered bond,' it functioned as a bearer bond, with unknown ownership, until cancelled eight months later, in October, 1969. We don't know exactly what happened, but it seems likely that the bearer sold the bond to someone else who traded it in for another registered bond. Whatever the situation, the transaction took place one year after the Pennsylvania Railroad merged with the New York Central and only eight months before it filed for bankruptcy protection.

Registered bond traded for bearer bonds.

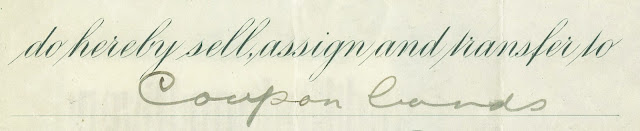

This $5,000 registered debenture bond was issued by the New York Central & Hudson River Railroad, August 20, 1925. Five days later, the bondholder exchanged the bond for five $1000 bearer bonds and the registered bond was cancelled. One can presume that the registered bond would have been traded for bearer debenture bonds of the same series. However, no such bearer bonds have yet been reported. Shown below is the transfer panel on the back. The handwriting and ink does not match any other writing on the bond, so we do not know who wrote the phrase 'Coupon bonds.' It seems possible that the instruction might have been written by someone at the bondholder's brokerage.

Transition from bearer status to registered status.

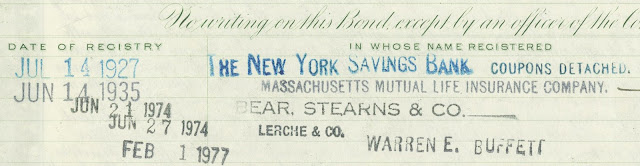

Shown below is part of the transfer panel on the back of a $1000 general mortgage bearer bond issued by the Cleveland Cincinnati Chicago & St Louis Railway in 1893, more popularly known as the 'Big Four.' The New York Central acquired control of the Big Four in 1906. While certainly underwritten by the giant New York Central, the company made its own interest payments on bonds like this and the company was a solid investment well over half a century. Between 1893 and 1927, the ownership of the bond is entirely unknown. However, the New York Savings Bank came into possession of the bond at some time during that period and converted it to registered status in 1927. During conversion, the bank surrendered all the coupons and thereby registered its interest payments with the railroad company. It appears the bank held the bond through the 1929 stock market crash and the worst of the Great Depression before selling it to Massachusetts Mutual Life Insurance in 1935. That company owned the bond for the next 39 years, during which time the New York Central merged with the Pennsylvania Railroad. The resulting Penn Central filed for bankruptcy protection in 1970, and Mass Mutual ultimately sold the bond to Bear, Stearns & Co. in 1974. Bear, Stearns re-sold the bond six days later to Lerche & Co. which held the investment for three more years. By that time, the bankruptcy had long been in litigation and the value of bonds like this dropped to around $40. A favorable outcome for investors was highly uncertain. Lerche & Co. ultimately sold the bond to Warren Buffet in 1977. The bond was retired and cancelled November 3, 1978, presumably as part of the Penn Central Transportation Company's bankruptcy court agreement of August, 1978. We don't know how much Buffet might have paid for the bond, but one can surmise he did not lose money.

Transition from bearer status to registered status and then back again.

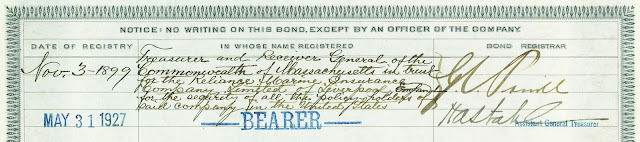

The New York Central & Hudson River Railroad Company issued this $1000 gold mortgage bond in 1897. After an unknown ownership for two years, the Commonwealth of Massachusetts registered this bond as an investment held in trust for the Marine Insurance Company of Liverpool. The bond stayed in the trust for the next 29 years, presumably netting $1,105 in interest. At that time, the new buyer converted the bond back to bearer status. Its history turned dark again and there is no record of who or what might have owned this bond during the Central's merger with the Pennsylvania Railroad in 1967, the bankruptcy of the Penn Central in 1970, or acquisition by Conrail in 1976. Whatever the case, the bond was ultimately retired, on Oct 31, 1978, only three days before Buffett's bond above, and probably for a similar amount. Once cancelled, it lived in the Penn Central archives until John Herzog convinced the Penn to sell its old paper securities instead of incinerating everything. Chances are, the bond sold as part of a large lot in a NASCA/Smythe sale in 1987 or 1988. I ultimately acquired the bond from Clinton Hollins in 2005.