Selling Debt - How Bonds Work

To anyone used to retail commerce, the idea of "buying debt" sounds somehow wrong. Ask the ordinary person invested in mutual funds or real estate to explain bonds and you will normally hear a degree of stuttering.

The simple answer is that bonds are certificates that represent debt. When good companies go bad, it is easier for bondholders to get repaid than hapless stock investors.

Size of the bond market

The American stock market represents about $46 trillion in equity. The amount invested in the bond market is equal to that or larger.

Creating ordinary debt

Bonds are easy to understand once collectors understand that debt can be bought and sold just like any other asset. Let's start with a simple story.

Imagine you own an old truck you no longer use. You own the truck, so you are, therefore, an "equity owner."

A family friend has a teenager who just earned a driver's license. The kid needs transportation, knows you have an extra truck, and makes you an offer of $2,000. You trust the kid (and the family). You make a deal to sell it for $100 a month over 20 months. You write up a short contract, the kid agrees, and gives you the first hundred dollars.

Just like most auto lenders, your contract specifies you keep the title to your truck until the debt is paid. The kid also agrees to keep the vehicle insured during that time. You and the buyer sign the contract. The teenager becomes a "borrower." Once you hand over the keys, you become a "lender" (also known as "creditor"). You no longer own equity, you own "debt."

Fast forward five months

You received five $100 payments during the first five months plus the original $100 down payment. If you were normal, you promptly spent the money on a hobby or food and drink. You learn that one of your friends has a near-new riding lawnmower for sale and you need one. He is willing to sell it for $1,000, but you don't want to take money out of savings. However, you still have a contract with an unpaid balance of $1,500. You'd rather have the lawnmower today than $1,500 spread over the next fourteen months.

It turns out, your friend has loaned money before and is willing to trade his mower for your contract. After all, he is familiar with the kid and his family and decides they are an acceptable risk. You trade your loan contract and truck title to your friend, and motor away on your riding lawnmower. You tell the kid to pay your friend instead of you. Everyone's happy.

After signing both the title and the contract over to your friend, you switched positions again. Your friend is became the creditor and you became an equity owner of a riding lawnmower. You just sold debt.

The bond market works the same way. Bonds represent debt that companies promised to repay. Over 500 billion dollars in debt is bought and sold in the U.S. every day.

Who writes the contact?

When you sold your truck to the teenager, you probably bought a pre-printed contract at an office supply store. Or maybe you purchased a contract from an online source that was legal in your state. Either way, you protected yourself against non-payment. You made sure the truck stayed insured and you kept the title in the event the kid stopped paying.

If you have ever purchased large assets and needed to borrow money, you know that lenders always slant their lending terms in their favor. Yes, state and federal laws compel banks, credit unions, and hedge funds to be "fair" to you. However, be certain that they are more fair to themselves than to you. Unless rank amateurs, lenders structure terms of repayment and interest in their favor. Borrowers always have the option of accepting those terms or going elsewhere. When dealing with "small" amounts of money, borrowers generally accept whatever terms lenders stipulate and rarely shop around for better deals.

Attitudes change when the amount of borrowed money climb into the millions or hundreds of millions of dollars. The more money involved, the more borrowers want to write the contracts to favor themselves. When that happens, lenders have the option of saying "yes" or "no." We move into the world of corporate bonding when large companies become borrowers and investors become lenders, .

Corporate bonding

Typical retail lending is about lending "small" amounts of money to huge numbers of borrowers where lenders write the terms of contacts. Typical corporate borrowing is much the opposite; it is procuring huge sums of money from large numbers of investors and companies. Borrowers like that usually write the contracts.

"My word is my bond" is the origin of the term. In the corporate world, the promise to repay is both literally and physically true. When companies write bonds, they are writing contracts. They state all the necessary features such as interest rates, collateral pledged, repayment dates, and interest payment dates. They also write the remedies in the case they fail to fulfill their promises.

When investors buy bonds, they are lending money to companies. Anyone who "buys" a bond is actually lending money. The bond, whether physical or electronic, is merely the promise to pay.

Corporate borrowing is greatly more complicated than buying cars, houses and boats, both in scale and in the ramifications for not paying. The process, though, is still about needing money, credit worthiness, and the ability to repay. Borrowers might be corporations or public entities. It doesn't matter. They all need to structure terms as favorably as possible to attract investors while doing as much as they can to protect their own financial health.

Large borrowing entities such as companies, cities, states, and even countries must cater to investors who have thousands of investing alternatives. Their terms must seem reasonable and fair to large numbers of investors. Those kinds of borrowers attract lenders (investors) by adjusting:

- amount of money needed

- interest rates offered

- numbers of years until repayment

- frequency of interest payments

- collateral guarantees

Large and stable borrowers have capabilities of offering additional incentives such as convertibility into other bond types, adjustability of rate, and premium allowances in the event of early retirement, etc. (See additional bond types at Glossary.)

Gold bonds

Inflation during the American Civil War (1861-1865) hit bond investors especially hard. Between 1860 and 1866, the dollar lost half or more of its value. (Estimation is difficult because of pronounced regional differences.) After incurring such large losses of value, bond investors became understandably concerned about lending money again without additional protections.

It was widely believed that gold would always retain an acceptably constant buying power. Corporations used that assumption and began promising to repay their bonds in gold coinage instead of ordinary currency. The earliest recorded railroad bond that promised to repay principal and interest in gold was issued in 1865. The number of gold-denominated bonds increased steadily until the Panic of 1873. That event radically dried up investments. A depression followed (at the time, popularly known as the Great Depression) and ground railroad expansion to a halt. Investments gradually recovered and the popularity of gold bonds increased even more.

Evidence from extant collectible bonds suggest more railroad gold bonds were issued in the 1890s than in any other decade. Surviving collectible bonds also suggest a diminishment after 1900, but that observation is not easily confirmable.

Trucking and another recession in 1920 siphoned off short-haul railroad traffic. In response, it appears corporations shortened repayment periods in order to attract more investors. The great Wall Street stock market crash of October, 1929 affected the entire planet and drove international gold prices higher than the fixed pricew of gold in the U.S. The difference in gold prices between the official fixed American price and variable global prices became a monumental problem for corporations.

Based on the numbers and types of bonds known to collectors, it appears that companies had denominated 87% of their railroad bonds in gold between 1890 and October, 1929. High international gold prices forced almost all countries to abandon their gold standards between 1930 and the end of 1932. At the same time, the U.S. continued to pay its foreign debts in gold at its immovable $20.67 price. Financiers could almost hear a giant sucking sound as gold poured out of Fort Knox.

Once we realize the huge problem the U.S. government was having huge paying its gold-denominated foreign debt, we can see the monumental problem facing corporations like railroad companies. By late 1932 and early 1933, the price of gold and the fluctuating world market had sometimes surpassed U.S. prices by 40%. Occasionally even more. In the face of dwindling U.S. supplies, how many railroads, if any, could have afforded to purchase gold on the open market to repay their bonds in metal?

On April 5, 1933, Franklin Roosevelt signed a presidential executive order that limited private ownership of gold to $100 as an effort to stymie hoarding of gold coinage. Two months later on June 5, 1933, Congress passed a law that abrogated (cancelled) every clause in every U.S. contract that specified repayment in gold. In other words, the government outlawed repayment of bonds in gold coinage.

Ultimately, the U.S. gave into world pressure. On January 30, 1934, the U.S. raised its standard price for gold from $20.67 per ounce to $35. (See more detailed discussion at Gold bonds and frauds.)

Collectors might find it confusing, but almost fifty railroad gold bonds are known dated after June 5, 1933. Those bonds are actually replacements for earlier bond issuances. Legally, bonds could not be paid in gold, However, bonds are considered legal contracts and, as such, it is illegal to change wording, even on replacement bonds.

Repayment contracts

Bond certificates represent the crucial terms of final contracts that companies devise. Anyone who has bought real estate is familiar with the bulkiness of typical home sales contracts. One can safely assume that bond contracts for many millions of dollars are more robust than can be represented on a single page. Therefore, bonds normally reference additional documents, typically mortgages, that are available for inspection upon request.

Selling debt to investors

Other than perhaps the reputations of corporate officers and treatments of passengers, railroads usually had mimimal relationships with private investors. Most companies needed "underwriters" to help sell their debt. Underwriters were typically large commercial investment banks, savings and loans, and trust companies. Their roles were to find sufficient numbers of corporate and private investors willing to risk money. Of course, underwriters were paid for their efforts. They frequently purchased entire bond issuances at discounts. Be assured that underwriters were also good at assessing the reality and risks of bonds issuances. They were definitely not going to buy hundreds or thousands of bonds without foreknowledge!

Re-selling discounted bonds were how underwriters made money. They were good at estimating how successful their selling efforts would be, given the terms presented to them by companies. A small number of specimen bond certificates are recorded in this database that show two certificates of identical design, generally varying in date and interest rate. The earlier bond probably proved inadequate to attract sufficient numbers of investors. The second was usually printed a year or two later with more attractive terms. Research would be needed to determine whether second sales attempts were more successful.

Re-selling discounted bonds were how underwriters made money. They were good at estimating how successful their selling efforts would be, given the terms presented to them by companies. A small number of specimen bond certificates are recorded in this database that show two certificates of identical design, generally varying in date and interest rate. The earlier bond probably proved inadequate to attract sufficient numbers of investors. The second was usually printed a year or two later with more attractive terms. Research would be needed to determine whether second sales attempts were more successful.

Investors' purchase prices

It is easy to assume that bonds were normally sold at denominations indicated on bonds. While many bonds certainly sold for face value (also known as "par value"), many more were not. Underwriters, institutional investors, and big-name investors often received volume discounts. Additionally, prices might have been lowered or negotiated in the face of market scares. Collectors will notice fewer bonds were issued during recessions and depressions and more during high-flying periods like the "gay nineties" and the "roaring twenties."

Repayment schemes

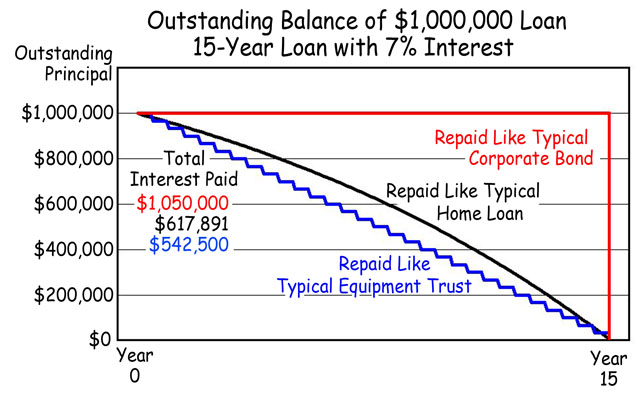

The vast majority of bonds in this project are loans of thirty years or more with interest rates in the range of 5% to 7%. They are considered "simple interest loans in that only interest is paid until principal is repaid in a lump sum at the end of the borrowing period. Since the entire of amount of principal remained unpaid over many year, typical corporations paid much more in interest than if those same amounts were repaid like typical home loans (Home loans are normally "amortized," meaning that both interest and some principal are paid every time a regular payment is made.)

In between the concepts of simple interest loans and amortized interest loans is a sub-group which includes Equipment Trust Certificates (ETCs) and "Serial Bonds." Those types of bonds repay principal as they go along, typically twice per year. Since those kinds of "instruments" regularly repay some principal and end up being much less of a drag on corporate finances.

Below is a chart that illustrates the differences between typical corporate bonds, ETCs (and serial bonds), and typical amortizing home loans.

This chart clearly shows that serial bonds repay principal the fastest. In doing so, serial bonds (ETCs) also spend the least on interest over the same 15-year period. Moreover, investors tend to consider those kinds of loans as safer investments, very much less prone to vacilations of the stock and bond market.

Almost exactly opposite are corporate bonds. Since they do not repay ANY principal until the end of bond terms, they are substantially riskier for investors. Yes, corporate bonds can always be bought and sold during the terms of loans, but that does not ameliorate ups and downs in the bond market. And from corporate perspectives, interest must be paid each and every time it is due, no matter how good or bad business might have been since the last interest payment. On the other hand, successful companies know how to plan for the effects of inflation. In fact, some companies consider inflation a benefit when delaying entire repayment of principal for fifteen of more years. If inflation averages only 2.5% per year over fifteen years, the company is repaying with money that is worth 32% less than when it was borrowed. As long as they can outpace inflation with income, delaying repayment can become a profit center for astute companies.